In the competitive landscape of capital markets, leveraging machine learning (ML) has become a critical differentiator. Success in this domain isn’t merely about deploying sophisticated algorithms; it fundamentally hinges on a strategic combination of three essential elements:

- Experienced Portfolio Manager: The role of a portfolio manager is paramount. They bring deep market insights and a strategic vision that align the ML project’s outcomes with broader investment goals. This ensures that the technology serves practical, profit-driven purposes rather than becoming an academic exercise.

- Top-Tier Data Scientist: A highly skilled data scientist is indispensable for navigating the complexities of AI and ML algorithms. Their expertise ensures that solutions are robust, scalable, and tailored to the specific nuances of financial markets. Their role is not just to implement algorithms but to understand which algorithms best suit the financial data’s nature and the investment goals.

- Expert Data Analyst: The quality of data is as important as the models themselves. An expert data analyst ensures the integrity of a state-of-the-art database filled with high-quality, reliable data. Accurate and clean data is crucial for meaningful analysis and model development, ultimately determining the success of the ML-driven strategy.

The Inovestor Case Study: Applying the Key Trio to Canadian Equity Portfolio Management

Our recent initiative at Inovestor Asset Management, utilizing data from Inovestor, a leading Canadian FinTech firm, serves as a case study of this success formula. We employed a statistical learning algorithm to craft a strategy that selects fundamental and momentum factors delivering superior returns. Here, the focus wasn’t on deploying the most complex algorithms available. Instead, the emphasis was placed on the quality of the data and the application of precise rules to avoid overfitting—ensuring that the models remained robust and applicable across various market conditions.

This approach reaffirms a crucial point: less sophisticated algorithms, when applied to high-quality data, often outperform more complex models built on poor-quality data. By adhering to these three pillars—strategic leadership, expert execution, and superior data quality—we demonstrated that these are the true drivers of machine learning success in capital markets.

Overview of the Machine Learning Project for Canadian Equity Portfolio Management

The project centered on using a statistical learning algorithm to create an effective strategy for selecting factors in constructing Canadian equity portfolios. By analyzing 42 factors across the S&P/TSX Composite Index, we pinpointed those with the highest predictive power. This comprehensive analysis ensured that our model could discern which factors significantly influenced stock performance over time, thus providing a solid foundation for constructing a high-performing portfolio.

To maintain model integrity and prevent overfitting—a common pitfall in ML projects—we implemented precise rules throughout the model training process. This careful calibration ensured that the model performed well not only on historical data but also when applied to unseen, out-of-sample data.

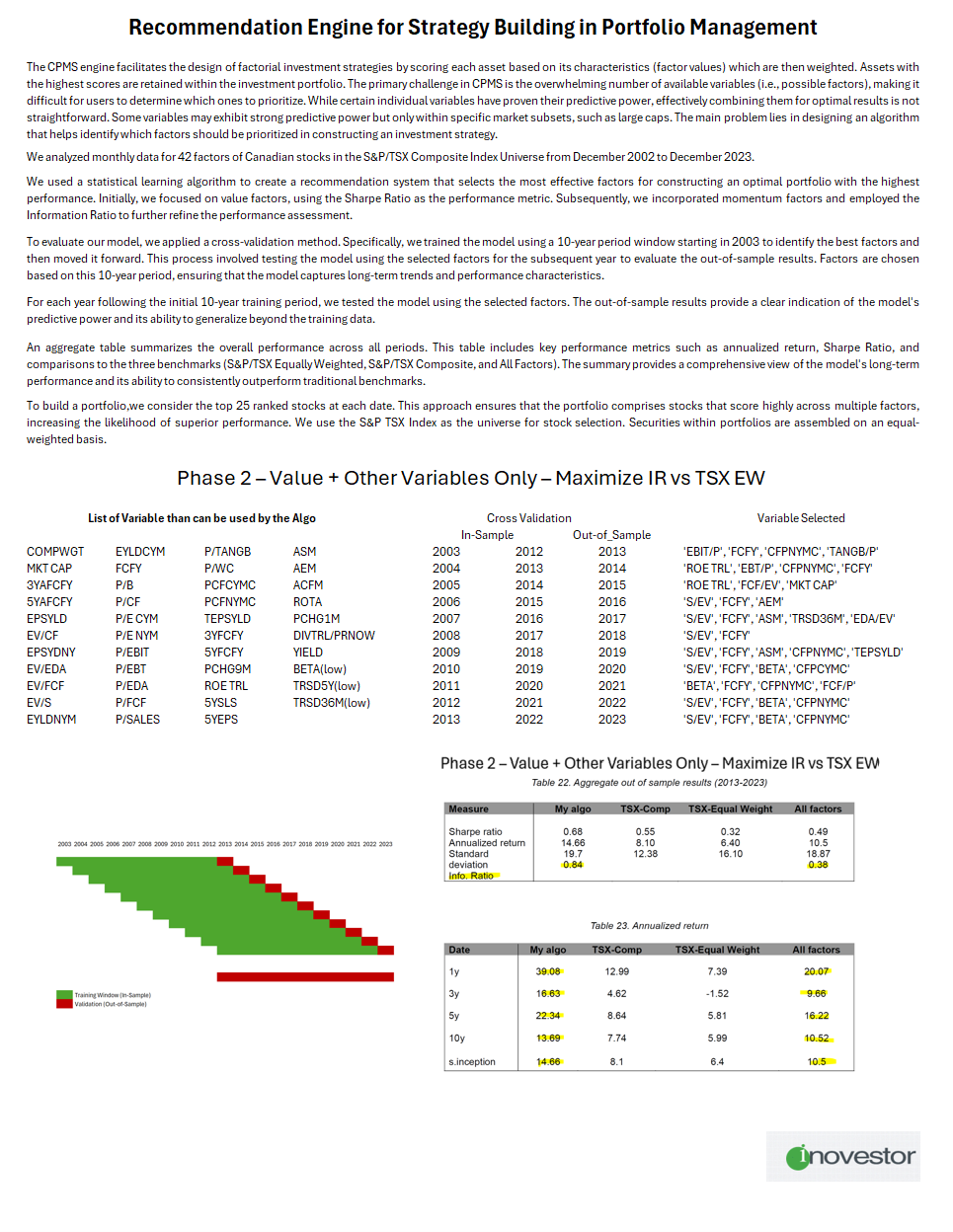

To build a portfolio, we consider the top 25 ranked stocks at each date. This approach ensures that the portfolio comprises stocks that score highly across multiple factors, increasing the likelihood of superior performance. We use the S&P TSX Index as the universe for stock selection. Securities within portfolios are assembled on an equal-weighted basis.

Results: Outperforming Traditional Benchmarks

The results from our rigorous evaluation process were impressive. Our model consistently outperformed (out-of-sample) traditional benchmarks, achieving a strong Information Ratio of 0.84 (versus S&P TSX equal-weighted) over an 11-year period. In comparison, the broader set of factors delivered an Information Ratio of only 0.49. This substantial difference underscores the value of our selective approach to factor analysis and model training.

Furthermore, the model delivered annualized returns of 14.68% over the same period, significantly surpassing the All-Factors benchmark. These performance metrics highlight not only the effectiveness of the factors selected but also the robustness of our statistical learning approach in optimizing portfolio performance.

Key Takeaways

This project’s success was driven by the collaboration of an experienced team:

- Karl Gauvin, Portfolio Manager: Provided deep market insights and strategic vision, ensuring the project aligned with investment goals and delivered actionable results.

- Parisa Davar, Data Scientist: Offered expertise in statistical learning algorithms, guaranteeing the models were both robust and scalable.

- Anthony Menard, Data Analyst: Managed the data pipeline, ensuring the integrity of the database and that high-quality, reliable data was available for analysis.

The Inovestor project serves as a testament to the effectiveness of a well-balanced approach in ML applications within capital markets. By leveraging the right combination of experienced leadership, technical expertise, and high-quality data, we have shown that machine learning can not only meet but exceed the demands of modern portfolio management. This model is now poised to deliver consistent returns and set a benchmark for future ML projects in the financial sector.

Conclusion: In the fast-evolving world of capital markets, staying ahead requires more than just adopting the latest technology. It requires a strategic approach, grounded in market expertise, technical proficiency, and data integrity. As the Inovestor case demonstrates, when these elements align, the results speak for themselves.