In our last Number Cruncher we discussed how Mastercard Inc. (MA:NYSE), W.W. Grainger Inc. (GWW:NYSE), & Choice Hotels International Inc. (CHH:NYSE) are companies that exhibit strong economic value-added (EVA) performance and operational excellence in their respective industries.

Let’s Begin with Mastercard Inc:

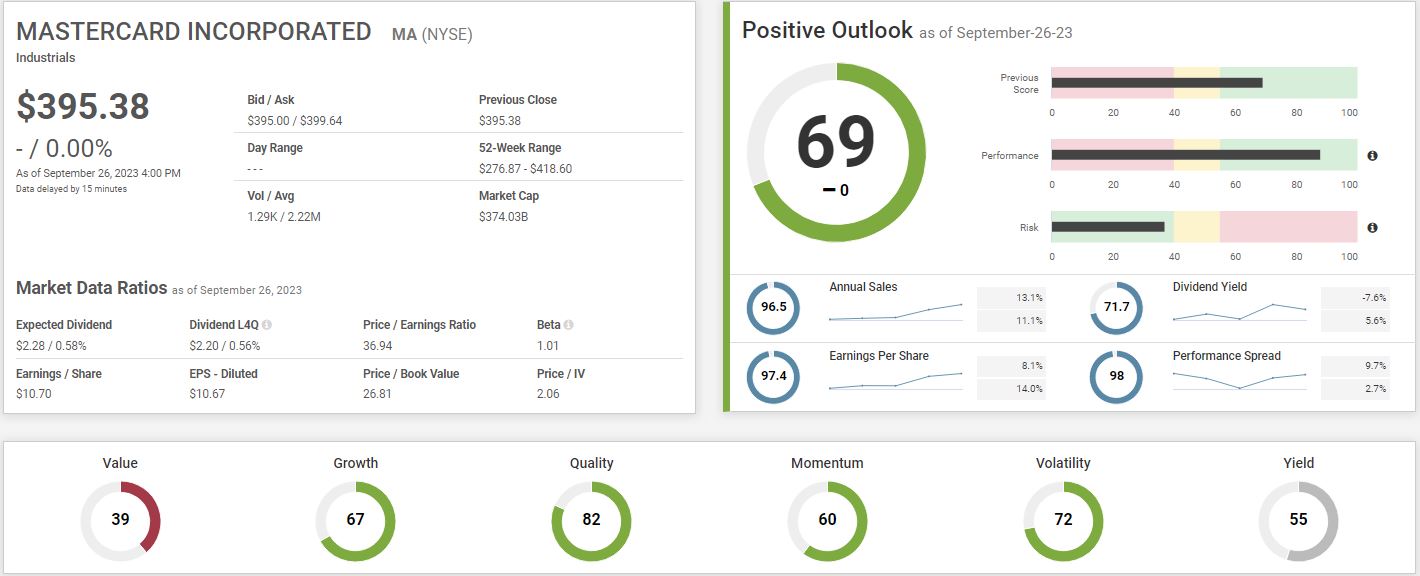

Mastercard Inc. (MA) currently maintains an SP Score of 69, a score it has held for the past 90 days. This composite score is derived from a Performance score of 88.1 and a Risk score of 37.1. Mastercard Inc. has demonstrated a modest 8.1% earnings growth. Furthermore, the company has exceeded expectations with a 1-year sales growth of 13.1%, surpassing its 5-year sales growth average of 11.1%. Mastercard Inc. also enjoys strong scores in growth, volatility, and quality metrics, highlighting its overall solid operational performance.

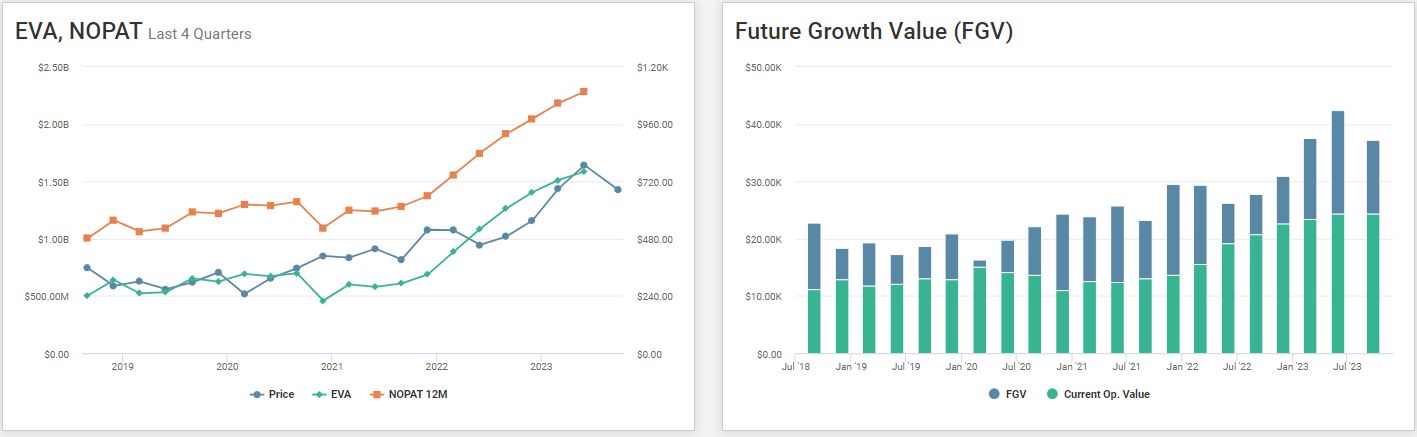

Recently, the company’s Economic Value Added (EVA) exceeded its stock price. Additionally, the stock price has exhibited a more rapid increase in comparison to both the company’s EVA and Net Operating Profit After Tax (NOPAT) over the last four quarters. When examining the company’s current operating value in recent quarters, it becomes evident that the company is still undergoing marginal growth in its operations. However, it’s worth noting that share prices increasingly align with this growth trajectory.

In light of these observations, it is advisable to exercise caution when considering an investment in this stock, as it is becoming less undervalued.

W.W. Grainger Inc.

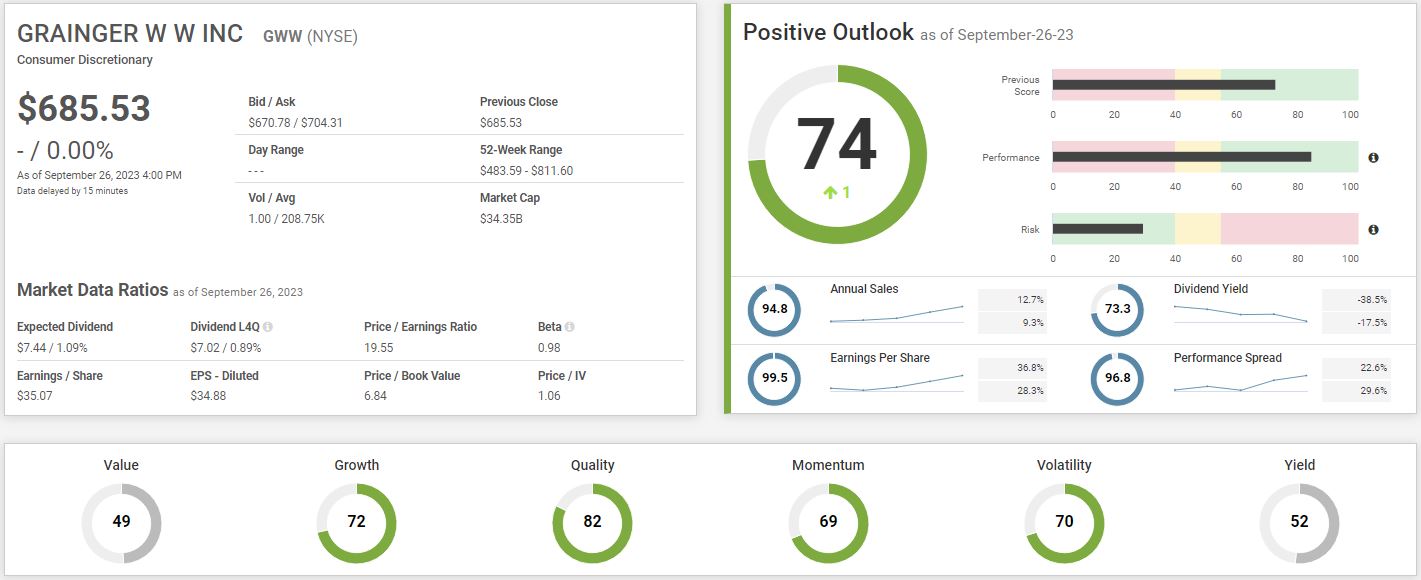

Grainger W W Inc. (GWW) currently boasts an SP score of 74, marking a one-point increase in the past 90 days. This score is supported by a performance rating of 84.6 and a risk score of 29.7. Notably, GWW has achieved the highest scores in quality (82), growth (72), and volatility (70) indicators.

In terms of earnings, GWW has consistently performed impressively with an average 5-year earnings per share growth rate of 28.3%. However, last year’s performance surpassed expectations with a remarkable 36.8% EPS growth. Similarly, the company’s average 5-year annual sales growth stands at a respectable 9.3%, but GWW’s recent year performance has exceeded this benchmark, achieving an impressive 12.7% sales growth.

Grainger W.W. Inc. had an impressive return on capital this year of about 28.3% and was able to maintain its 5Y average of about 21.7%.

Over recent years, both NOPAT and EVA have exhibited consistent growth trends, with the stock price closely tracking these patterns. In the last quarter, the stock price briefly matched the EVA before experiencing a slight decline. The company’s FGV has generally been on an upward trajectory in past quarters, although there was a minor decrease in the most recent quarter. It is advisable to carefully monitor these trends as the stock price approaches its EVA.

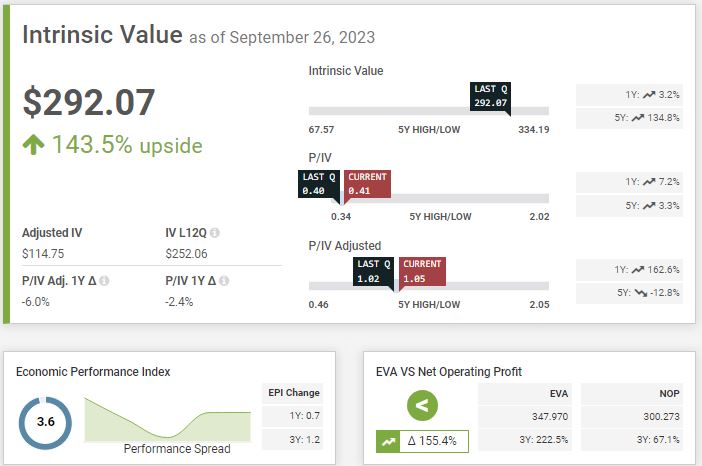

Choice Hotels International Inc.

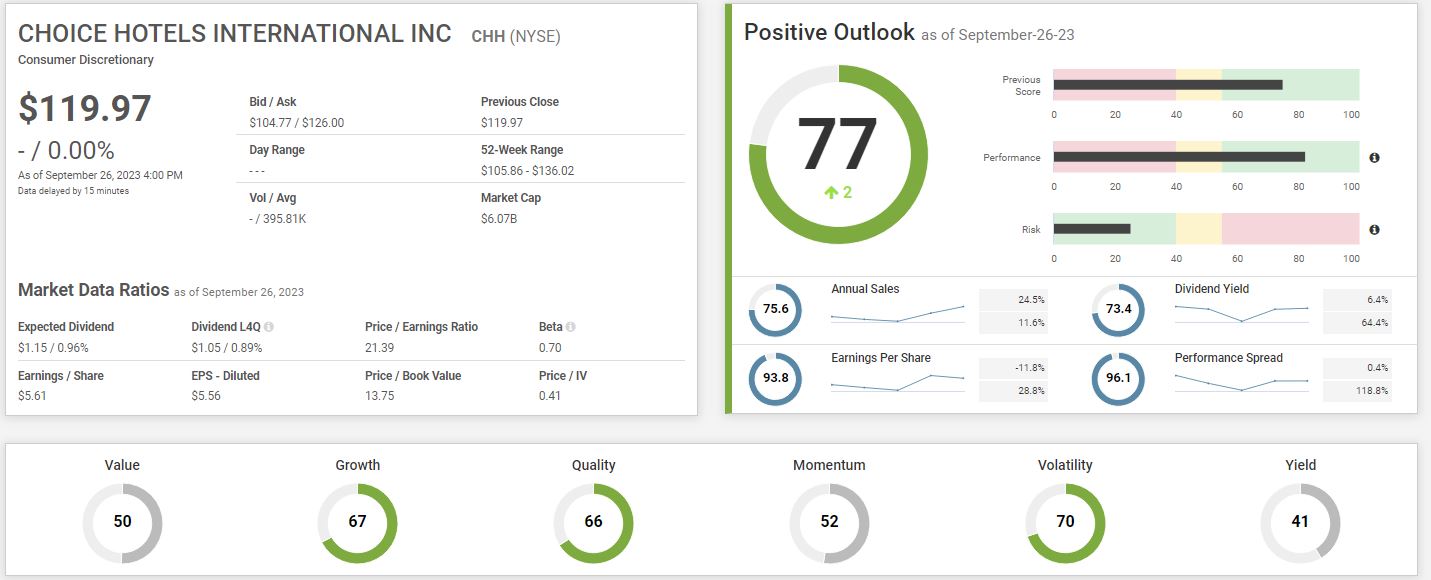

Choice Hotels International Inc.’s SP score rose by 1 point in the last quarter, reaching a score of 77. It’s important to note that the company’s EPS declined by 11.8%, a noteworthy deviation from its 5-year average of 28.8% in EPS growth. Conversely, Choice Hotels International Inc. demonstrated substantial sales growth of approximately 24.5% in the previous year, exceeding its 5-year sales growth average of 11.6% by more than two-fold.

The company has effectively sustained its Net Operating Profit After Tax (NOPAT) at a relatively consistent level over the past five quarters. Moreover, an analysis of the Financial Growth Value (FGV) histogram graph indicates that the company’s operating value is in close proximity to converging with the market-estimated value. This convergence is attributed to the gradual and modest increase in the stock price observed over the past year.

The company has consistently delivered impressive results, with an average 3-year Economic Value Added (EVA) growth rate of 222.5% and an average 3-year Net Operating Profit of 67.1%. If the ongoing upward trend in these metrics persists and the company also demonstrates revenue improvement, our estimation indicates a potential upside of approximately 140.8%. This suggests that the company may present an attractive investment opportunity worth considering.

If you have any questions about the article, feel free to contact Anthony :

amenard@inovestor.com