In our last Number Cruncher, we discussed how Dick’s Sporting Goods Inc. (DKS:NYSE), PNC Financial Services Group Inc. (PNC:NYSE), & Snap-on Inc. (SNA:NYSE) are companies that provide a combination of steady dividend growth, low payouts, and respectable yields.

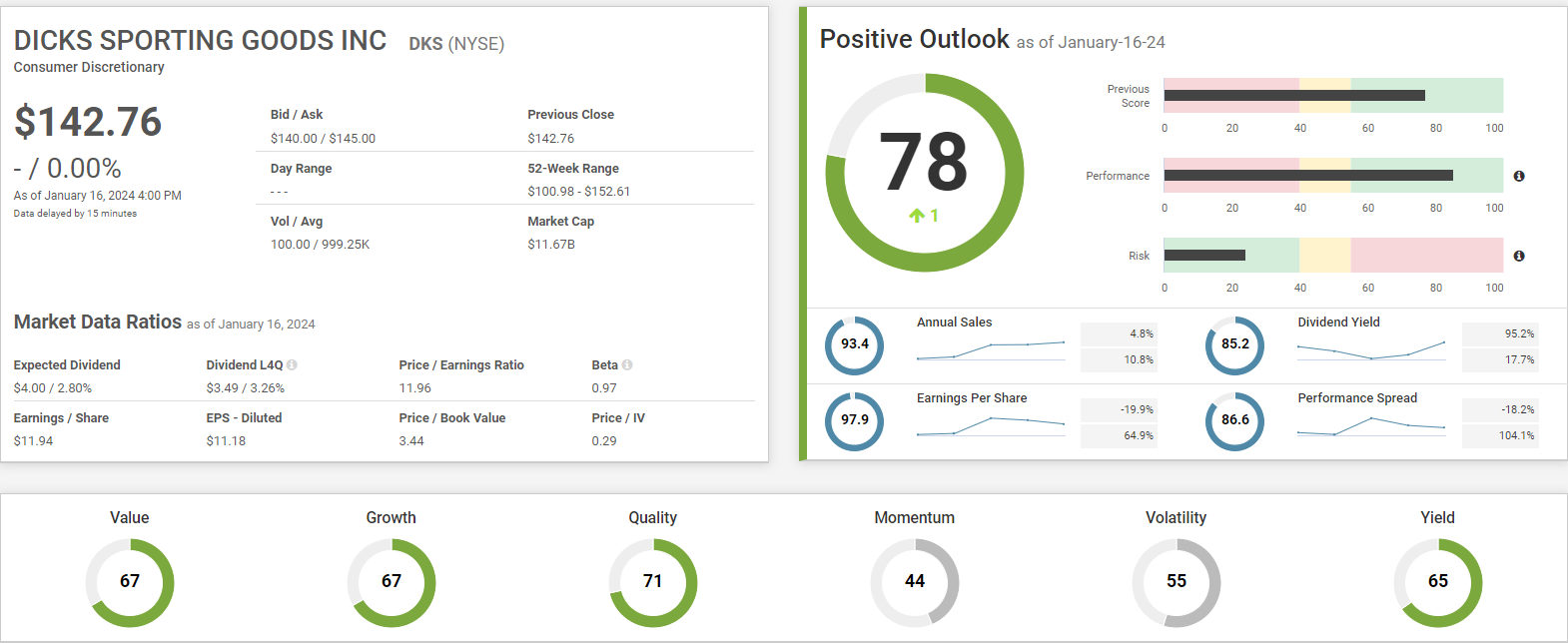

Dick’s Sporting Goods currently has an SP Score of 78, a one-point increase in the past 90 days. The score is comprised of a strong performance score of 85.4 and a risk score of 24.1. DKS stands out primarily for its quality (71) and growth (67).

The dividend yield growth has significantly exceeded it’s 5-year average of 17.7% with 95.2% yield growth in the past year. Annual sales, however, have slowed down with 4.8% annual growth compared to the 10.8% average in the past 5 years.

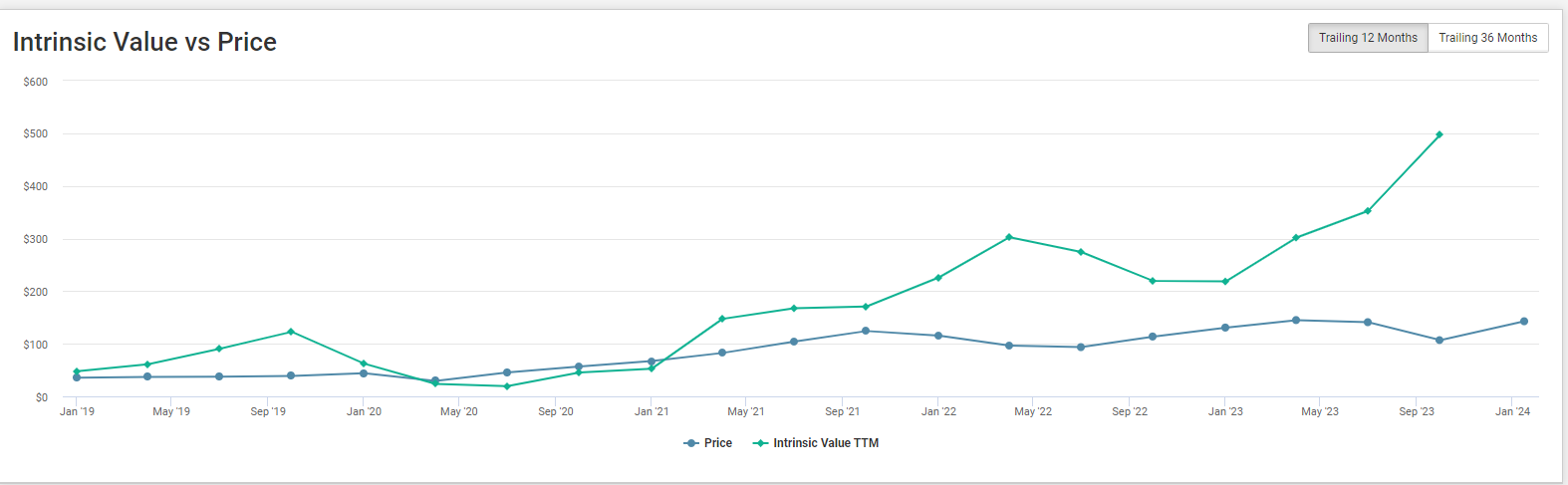

When comparing the DKS stock price to our intrinsic value estimates, the estimates have been greater than the stock price since early 2021. However, the intrinsic value estimates have grown significantly in the past 4 quarters, whereas the stock price has remained consistent, demonstrating an increase in value for shareholders. These estimates are surprising considering they have continued to increase since the surge in demand for sporting goods during the COVID-19 pandemic and are yet to decrease or stabilize near pre-pandemic levels.

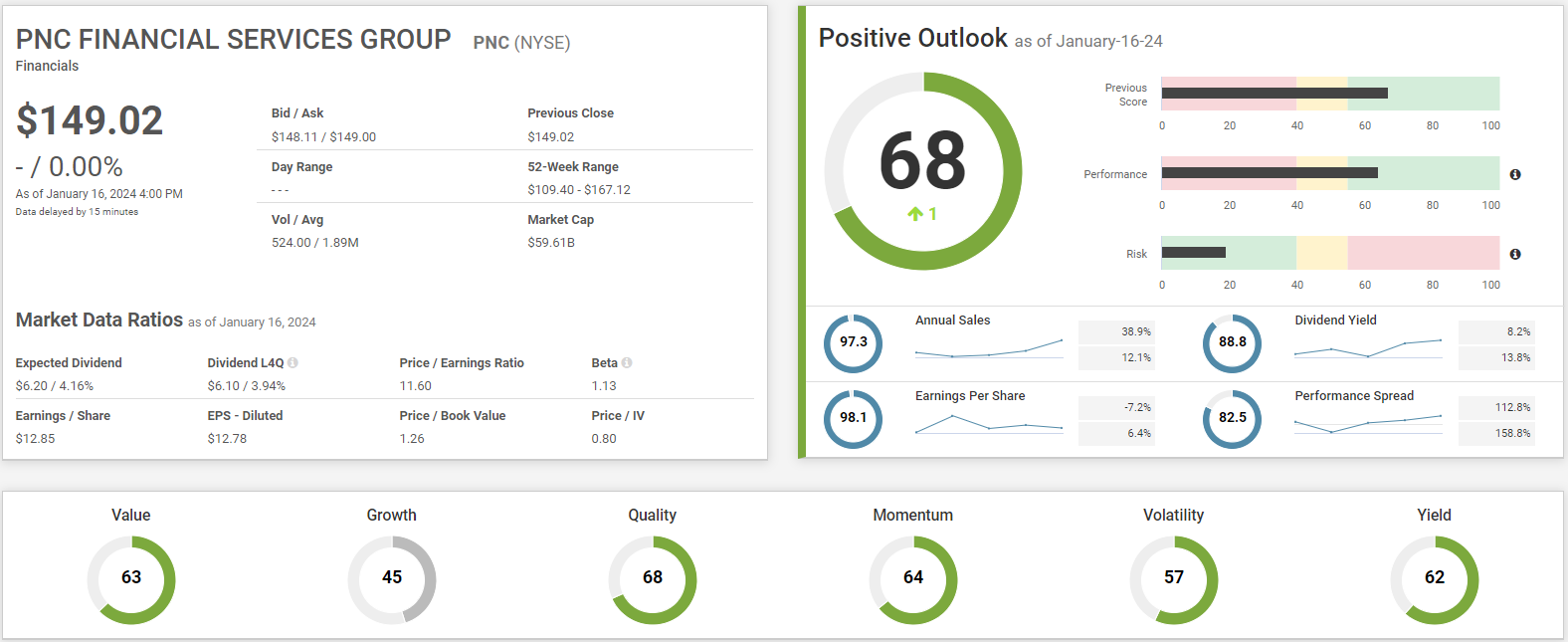

PNC Financial Services’ SP Score rose by 4 in the past 90 days and currently stands at 70. The score encompasses a performance score of 66.9 and a risk score of 19.5. This financial company’s strongest factor compared to its peers is its value at 78. Other positive factors include yield and quality, scoring 68 and 67 respectively. PNC’s lower scoring factors compared to other financial companies are growth and volatility.

In the past year, annual sales have increased by 49.8% which is significantly higher than their 5-year average of 10.5% growth, likely due to higher interest rates. Additionally, the 5-year average earnings per share growth is very strong at 17.7%, although last year has been below the average growth at 8.7%.

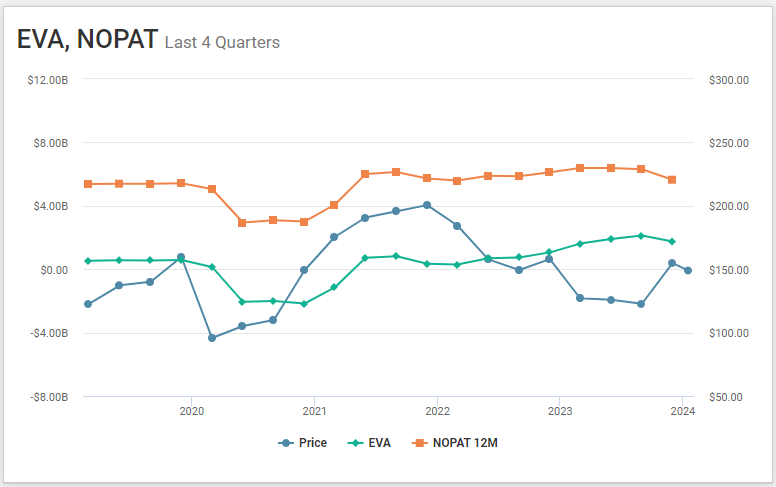

PNC’s economic value added (EVA) and net operating profit after tax (NOPAT) have performed similarly in recent years. Price, however, had underperformed these metrics at the beginning of last year until its recent growth since September. As the price declined, EVA continued to see sustained growth for the past 2 years, which should positively impact PNC’s price going forward.

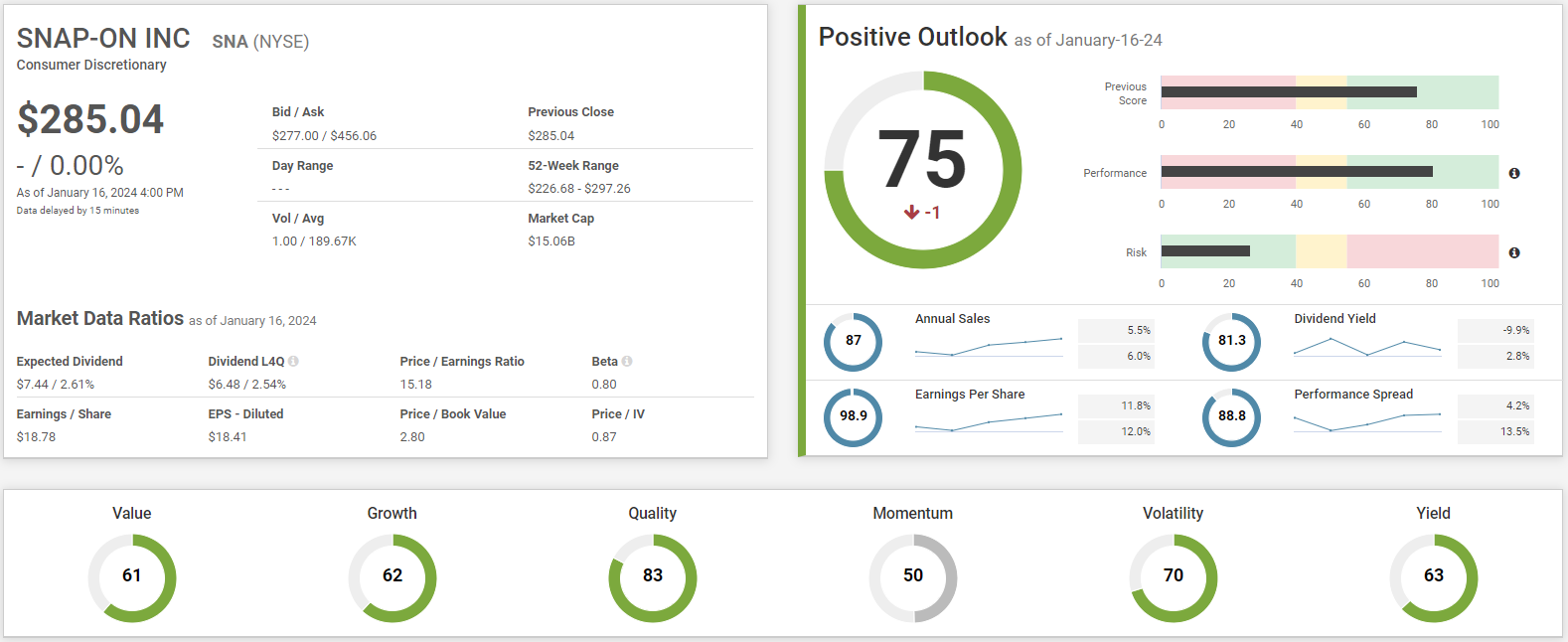

Snap-On currently has an SP Score of 75, a one-point decrease in the past 90 days. Its SP Score is in part comprised of a performance score of 80.5 and a risk score of 26.6. The company has been very consistent with an annual sales growth of 5.5% compared to a 6% average in the past 5 years and an annual EPS growth of 11.8% compared to a 12% 5-year average. This is also demonstrated in its volatility, scoring 70. Additionally, the strongest factor when compared to other consumer discretionary stocks is its strong quality score of 83.

Snap-On’s current operating value has consistently increased in recent years with a total increase of 36.8% in the past 3 years. Additionally, its future growth value has been positive and increasing for over a year, currently sitting at 18.2%. The company’s EPI is currently 2.0 which ranks in the 86th percentile in its sector. These factors continue to demonstrate strong value for shareholders. However, the factors could indicate that the valuation is relatively high.

If you have any questions about the article, feel free to contact Anthony:

amenard@inovestor.com