In our last Number Cruncher, we discussed how Consolidated Edison Inc (ED:NYSE), WEC Energy Group (WEC:NYSE) & Entergy Corp. (ERT:NYSE) are utilities companies with robust economic performance that might see heightened demand fuelling their growth.

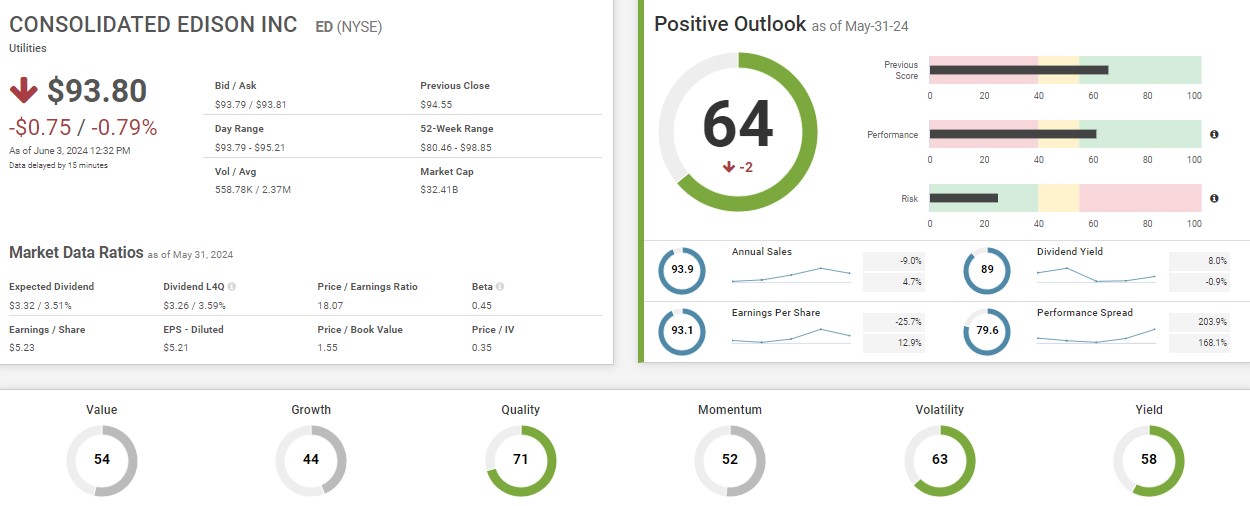

Consolidated Edison (Con-ED) currently has an SP Score at 64, comprising a Performance Score of 61.45 and a Risk Score of 25.35. Con-ED’s strongest factors compared to its peers are Quality and Volatility. The company experienced an incredible 203.9% performance spread growth, and the 5-year average performance spread growth of 168.1%. Performance spread indicates company’s ability to generate value over its cost of capital thereby showcasing value creation for shareholders.

The intrinsic value chart depicts an exponential increase in the intrinsic value of the company over the last year. Our estimation shows that the company was overvalued between January 2022 and June 2022. Since June 2022 the company has been undervalued. It can be seen to be creating value as shown by its performance spread increase, growing its intrinsic price, and widening the gap with its market price in all the subsequent quarters. Con-ED continues to be a strong utilities company leading its peers at a compelling valuation.

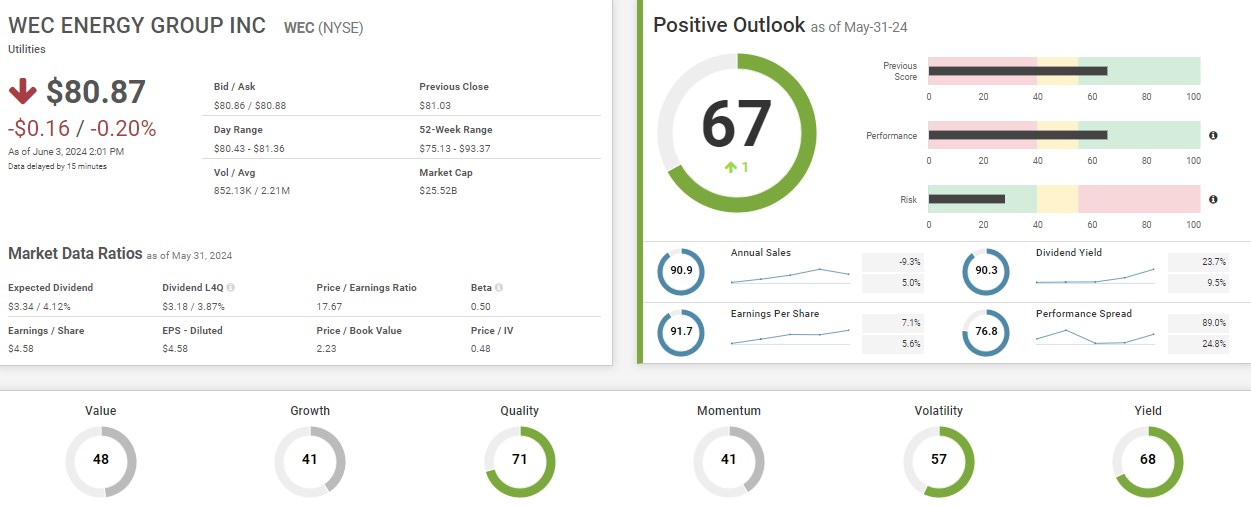

WEC Energy Group Inc currently has an SP Score of 67 which has increased by 1 in the past 90 days. The SP Score is based on a performance score of 65.9 and a risk score of 28.2. Currently, WEC Energy Group top factors are quality, scoring 71, and yield, scoring 68. The company had an earnings per share growth of 7.1% and EPS 5-year average growth of 5.6%. The company had an impressive growth in dividend yield of 23.7% and has a 5Y average of 9.5%.

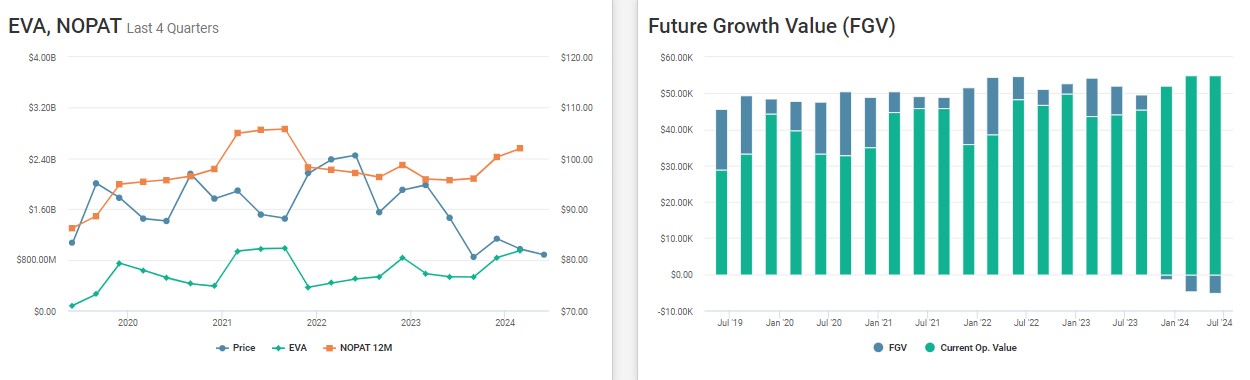

The EVA and NOPAT graph for the last 4 quarters exhibits the company’s increasing NOPAT. Notably, their net operating profit after taxes (NOPAT) has increased in the last two quarters going from 2.1 billion in June 2023 to 2.5 billion in March 2024 and has successfully discontinued its slightly declining NOPAT trend over the last two years. EVA has also grown in the last two quarters.

The future value growth graph reflects to be the lowest in the past couple of years which can be explained through the declining share price over the past years and a low cost of capital for a utility company. The NOPAT trend, and the increasing EVA value with a negative FGV can be used in consonance to estimate that the company is current trading at an undervalued price.

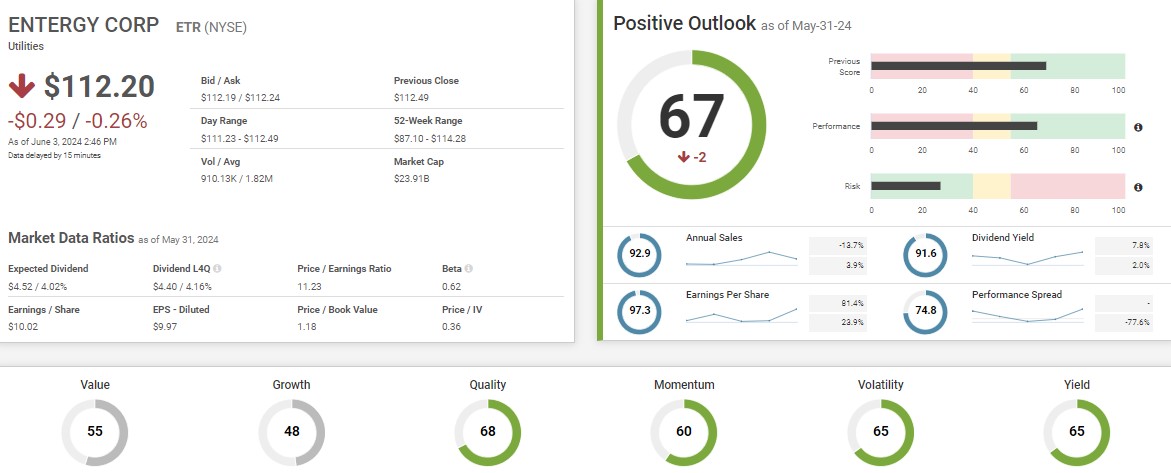

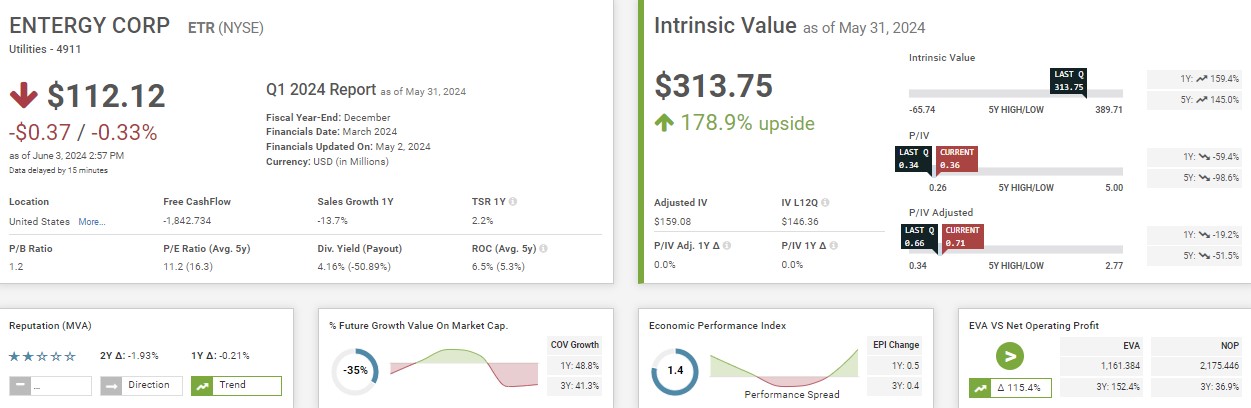

Entergy Inc current SP Score is 67 (comprising performance score of 65.4, risk score of 27.4). The company’s strongest factors compared to its peers are quality and yield with respective scores of 68 and 65. Entergy’s price to earnings ratio is 11.23, lowest among its peers. It also has an impressive the price to intrinsic value ratio of 0.36.

Entergy’s economic performance index is 1.4x and ranks in 78th percentile in its sector, indicating an impressive spread of ROC over the cost of capital. StockPointer estimates the value of the stock at the price of $313.75 (178.9% upside). Investors should be cautious of the negative sales growth of 13.7% last year. With a strong EPI and a wide spread between market price vs intrinsic value shown by a low price to IV of 0.36, we estimate the stock to be undervalued and give it a buy recommendation.

If you have any questions about the article, feel free to contact Anthony:

amenard@inovestor.com